Does it happen that your monthly paycheck does not cover your expenses? Do you know how much you spend on food, travel or rent every month?

For finances to work properly in the family (or with an individual), it is necessary to have your own budget. It means, you know the income and expenses of the whole household.

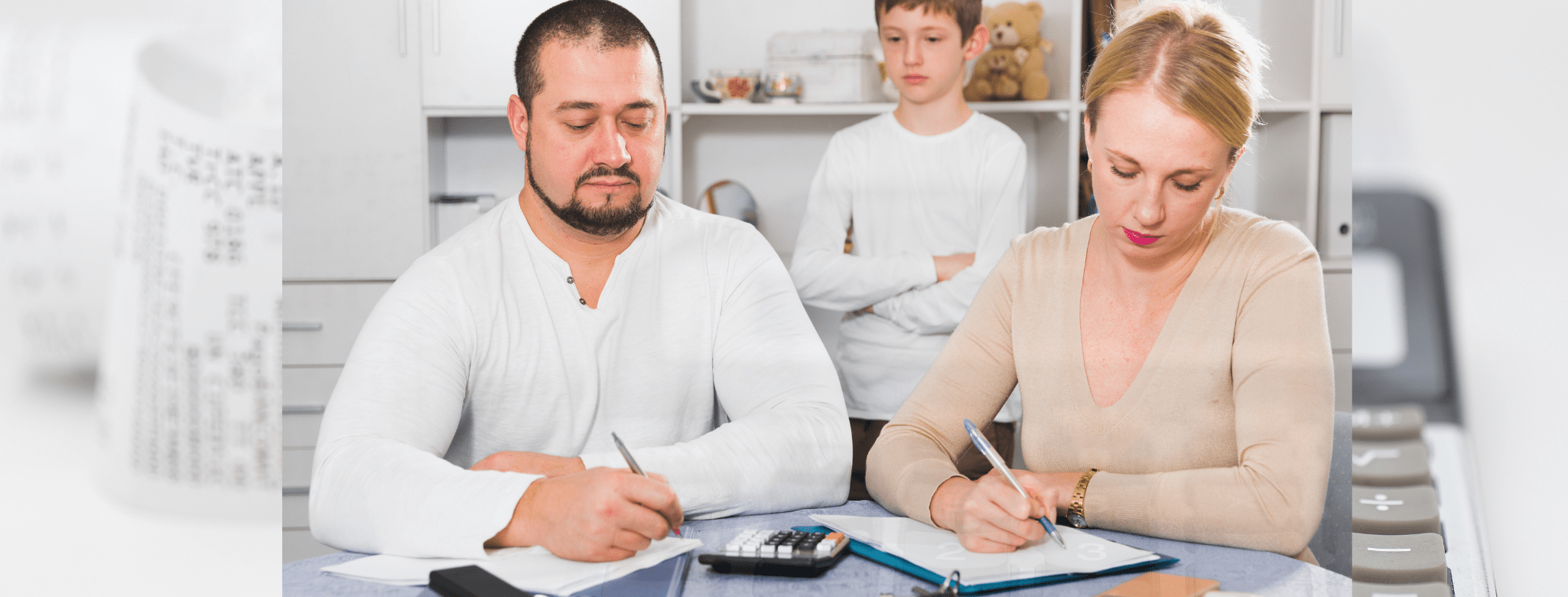

Sit down at a table, grab a pen and paper, and start writing down all your income and expenses.

The basis of household income is usually your salary or income from your business, social income (from government), or financial income (interest, dividends).

Household expenses consist mainly of payments for food and clothing, rent, electricity, car, TV, or repayments of mortgage and other loans, expenses for entrepreneurship, creation of emergency fund, etc. But don’t forget about holiday costs, gifts, concerts and similar expenses.

Once you are done with listing, make a line at the end of the paper and calculate the pluses (income) and minuses (expenses). The result can be either:

1. Minus

2. Plus

3. Balanced, i.e. close to zero

Each month, it is essential to cover the necessary regular expenses in the first place, such as rent, electricity, loan repayments, food, transport, insurance, etc., and also to include the creation of an emergency fund. And from what you have left, you can spend on culture, holidays, restaurants, etc.

If you find out that your income does not cover all your expenses (option A), you’ll have to review your expenses and stop spending money on unnecessary stuff.

If you find out that your income does not even cover the necessary regular expenses, you have 2 options: Either seek to increase your income, for example to get a better paid job, or a second job (which may not be easy); or you will need to reconsider i.e. reduce your spending. For example, you can pay lower rent if you move to a smaller apartment or further from the city center. What installments do you have to pay every month? For example, if you can’t cover your car installments and gas payments, it may be wiser to sell the car and use public transportation.

On the contrary, if you have higher income than expenses every month (option B), it is smart to think about a certain form of savings or investment. Money in the current account loses value, but mainly it does not earn any profits.

After all, there should be consistency between income and expense, i.e. they should be at the same level, balanced (option C).

Everyone should be creating an emergency fund. It is recommended to put at least 10% of your income into a fund until the fund reaches the amount of approximately 6-month salary (income). It is intended to cover unexpected expenses or loss of income. The creation of an emergency fund should be included into your regular monthly expenses. If you have an unstable income, e.g. from business, or you may lose your job, then it is especially necessary to create a larger emergency fund.

I wish you good luck in balancing your family budget. If you still have something extra left at the end of the month, you may be able to help people in need, contribute to charity, or support various non-profit organizations. They will be grateful for any contribution, ideally if you can include it into your monthly budget and contribute regularly.